By Buchanan Maldonado

When the Federal Reserve says QE is on the horizon typically that means it stops shrinking its balance sheet and begins buying assets again (Treasuries, MBS, etc.)—the real estate market typically reacts in several predictable ways. These effects are based on past cycles (2008–2015 QE, 2019 repo interventions, the 2020 QE surge), and while not guaranteed, they follow well-observed patterns.

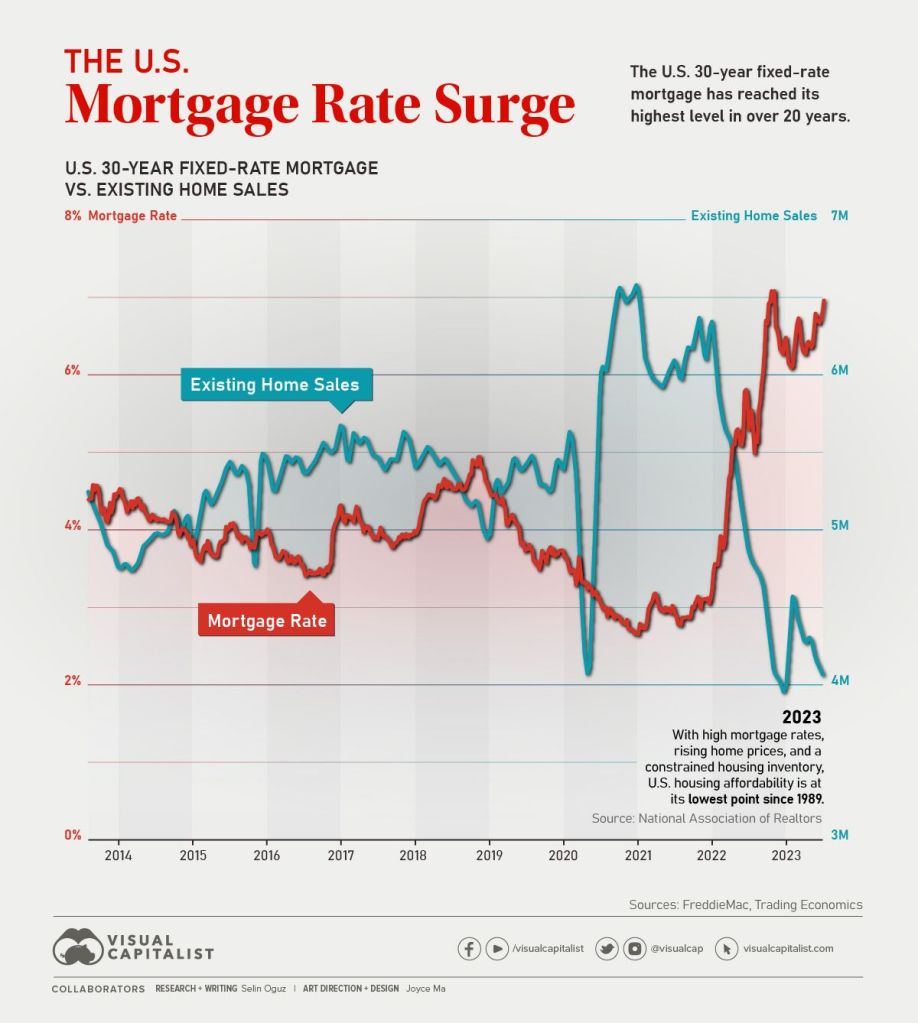

🔵 1. Mortgage Rates Usually Fall (Sometimes Rapidly)

When the Fed buys mortgage-backed securities (MBS) or Treasuries, demand increases for these assets. That demand pushes yields downward, which directly reduces:

Treasury yields (10-year) → foundation for mortgage rates

MBS yields → directly lowers mortgage interest rates

What this means for real estate:

✔️ Lower mortgage rates increase buyer affordability

✔️ Home-buying demand rises

✔️ Refinancing booms return

✔️ Homeowners who were locked out by high rates re-enter the market

This is typically the fastest-moving effect—rates react almost immediately.

🔵 2. Home Prices Usually Rise—Sometimes Sharply

Lower rates + reduced borrowing costs = more buyers able to bid.

QE often leads to:

Increased buyer competition

Price appreciation in both entry-level and luxury segments

Faster sales cycles

Reduced inventory as more buyers chase the same homes

Historical examples:

QE1–QE3 (2009–2015): Home prices nationally rose double digits in many markets.

2020 QE surge: U.S. home prices rose over 40% in 24 months, the strongest price boom in modern history.

QE inflates all asset classes, but housing tends to respond the strongest because it is credit-sensitive.

🔵 3. Real Estate Investment Activity Expands

When money becomes cheaper and liquidity increases, investors return aggressively:

Institutional buyers ramp up purchases

Single-family rental funds expand

Fix-and-flip investors re-enter

Commercial real estate financing becomes easier

QE revitalizes risk appetite, pushing capital back into real estate.

🔵 4. Construction and Development Activity Increases

Lower borrowing costs → cheaper financing for developers.

QE often improves:

Housing starts

Multifamily development

Commercial project financing

Permitting activity

Builders become more optimistic because lower rates mean more qualified buyers.

🔵 5. Equity Markets Rise → Wealth Effect Boosts Housing Demand

QE inflates financial assets such as:

Stocks

Bonds

Real estate investment trusts (REITs)

When households feel wealthier due to stock market gains, they are more willing to:

Buy second homes

Move up into larger homes

Invest in income-producing properties

The “wealth effect” plays a major role in boosting real estate demand during QE cycles.

🔵 6. Credit Conditions Loosen

Banks prefer to lend when:

Liquidity is abundant

The Fed is supporting credit markets

Risk appetite is high

You typically see:

✔️ Easier mortgage approvals

✔️ Lower down-payment programs gain traction

✔️ More HELOC and cash-out refinance activity

✔️ Commercial lending standards relax

🔵 7. Inflation Pressures Sometimes Increase (But Lagged)

QE can stimulate:

Housing price inflation

Rent inflation

Construction cost inflation

While inflation can drag on affordability eventually, in the short term QE overwhelmingly boosts real estate activity.

🔵 8. Psychological Shift: Market Sentiment Turns Positive

Just the announcement that QT is ending can trigger:

Lower rate expectations

Buyer urgency (“Before prices go up again…”)

Investor re-entry

Builder confidence rebounds

The Fed doesn’t even need to act aggressively—the pivot alone shifts market psychology.

🟢 What Typically Happens to Real Estate During QE

Typical Effect of QE

Mortgage Rates ⬇️ Fall quickly

Home Prices ⬆️ Rise

Buyer Demand ⬆️ Increases strongly

Inventory ⬇️ Tightens

Investment Activity ⬆️ Expands

Refinancing ⬆️ Spike

Construction ⬆️ Ramps up

Market Sentiment Turns bullish

Real estate is one of the biggest beneficiaries of QE cycles & a home purchase is one of the biggest financial decisions you’ll make. That’s why it’s essential to understand not just the mortgage — but the insurance costs that secure the roof over your head. When you work with a professional like me, you’ll know what coverage you need, what risks to look for, and how to avoid overpaying.

Let me help you protect what matters most: Quote.BuchananMaldonado.com.